Powerball Jackpot Soars To $1.7 Billion

The U.S. Powerball jackpot has climbed to an astonishing $1.7 billion, setting the stage for a record-setting Christmas Eve drawing that has captured attention nationwide. The latest round of play produced no jackpot winner, allowing the prize to swell further after Monday night’s drawing. Several tickets matched five numbers to secure million-dollar wins, but the grand prize remains unclaimed — and growing. The odds of winning remain extraordinarily slim, roughly 1 in 292 million, yet the holiday timing has fueled ticket sales and renewed enthusiasm. Winners will ultimately face a choice between a long-term annuity paid out over decades or a one-time cash option estimated at just over $780 million, a sum that would instantly reshape any financial reality. The current jackpot ranks among the largest in U.S. lottery history, joining a short list of billion-dollar Powerball runs that have captured the public imagination. In a year marked by economic uncertainty and rising costs, the swelling jackpot has become a shared moment of optimism — a reminder of possibility, however remote. Beyond the headline figure, the extended rollover highlights the unique tension at the heart of lottery culture: the promise of sudden transformation set against the certainty of long odds. With the next drawing scheduled for Christmas Eve, millions of Americans may head into the holiday holding a ticket — and a fleeting sense of what-if — as the year comes to a close.

Democrats & Republicans Pitch Competing Plans to Tackle America’s Affordability Crisis

As the cost of living continues to stretch household budgets, lawmakers on Capitol Hill are rolling out competing proposals aimed at lowering expenses for millions of Americans. With affordability emerging as one of the dominant political issues heading into 2026, both parties are trying to claim the mantle of economic relief — but with sharply different approaches. Democrats are pushing a plan centered on reducing out-of-pocket costs for everyday essentials, including efforts to lower prescription drug prices, expand housing assistance and boost subsidies for child care. They argue that household budgets have endured years of inflation-driven pressure and need immediate, direct support. Republicans, meanwhile, are prioritizing tax relief and deregulation. Their proposal focuses on easing federal rules they argue drive up prices, while offering targeted tax credits aimed at working families and small businesses. GOP leaders say the fastest way to bring down costs is to reduce the government’s footprint and spur private-sector growth. Households Still Feeling the Strain Despite slowing inflation and brighter economic indicators in some areas, many Americans say their financial stress hasn’t eased. Rising rents, higher insurance premiums, lingering food costs, and elevated interest rates continue to weigh heavily on families — especially lower-income consumers who face the steepest trade-offs. A Political Battle With Real Stakes With both chambers looking ahead to a contentious 2026 election season, lawmakers are racing to present solutions that resonate with voters. While the two plans share the same goal — improving affordability — the divide over how to get there has set the stage for months of negotiations. For now, Americans are watching closely, hoping the gridlock breaks and real relief finally reaches their wallets.

Tesla Shares Surge on Confirmation of Driverless Robotaxi Testing

Tesla shares jumped sharply Monday after CEO Elon Musk confirmed the company is testing fully driverless robotaxis on public roads without onboard safety monitors, a development that reignited investor optimism around Tesla’s long-term autonomous vehicle ambitions. The stock climbed to its highest level in nearly a year, reflecting renewed confidence among traders and long-term shareholders who see autonomous technology as a key driver of Tesla’s future valuation. The surge pushed the company’s market capitalization higher as investors reacted to what they viewed as tangible progress toward full autonomy. Tesla’s robotaxi initiative is central to Musk’s broader vision of transforming the company beyond electric vehicle manufacturing and into a leader in autonomous transportation and robotics. Earlier testing phases included human safety monitors, making the confirmation of unsupervised testing a significant milestone in the program’s evolution. Still, analysts remain divided. While advances in autonomy continue to fuel bullish expectations, concerns around electric vehicle demand, regulatory hurdles, and execution risks persist. Monday’s rally underscores how quickly market sentiment can shift when Tesla signals progress on its most closely watched technologies.

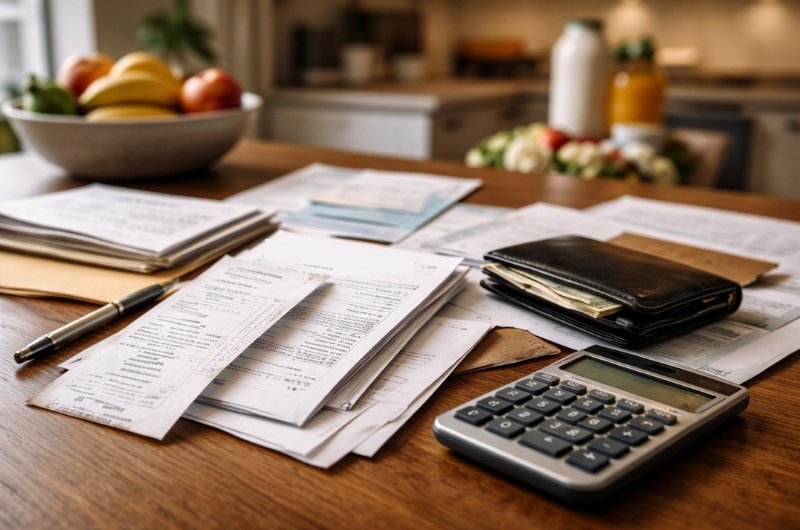

IRS Staffing Shortages Could Make the 2026 Tax Season a Rough One

As Americans prepare for the upcoming tax season, growing concerns are emerging over the Internal Revenue Service’s ability to handle the workload. Deep staffing reductions across the agency, including reports that some departments are operating with as little as one-third of their normal workforce, are raising red flags about delays and service disruptions in 2026. The IRS has lost a significant number of employees over the past year through retirements, buyouts, and budget-driven cuts. While workforce reductions have affected the agency broadly, internal operations tied to taxpayer assistance, return processing, and backend support have been hit particularly hard. The timing is notable, coming just as tax filings are expected to rise and rules continue to grow more complex. Fewer staff members could translate into longer wait times for taxpayers seeking help, slower processing of returns, and delays in issuing refunds. Call centers may struggle to keep up with demand, and taxpayers facing issues or errors could find it harder to reach a live representative during critical filing windows. The strain may also extend beyond customer service. Reduced staffing could limit the agency’s ability to conduct audits, resolve disputes, and manage compliance efforts efficiently, potentially affecting both revenue collection and enforcement consistency. For taxpayers, the message heading into 2026 is one of caution and preparation. Filing early, double-checking returns, and avoiding last-minute submissions may become more important than ever as the IRS navigates a tax season with fewer resources and rising demands.

Why Falling Inflation Still Isn’t Showing Up in Everyday Household Budgets

Inflation has eased from its recent highs, and in some cases, prices are clearly coming down. At one point, the price of eggs felt like a runaway train, racing ahead of household budgets and turning a basic necessity into a talking point. Now, we’re seeing eggs priced under two dollars a dozen. But for many households, that hasn’t translated into a real sense of financial relief. The reason is simple: while certain items have become more affordable, the underlying cost structure of daily life is still elevated. Housing, insurance, utilities, healthcare, childcare, and interest payments continue to consume a larger share of household income than they did just a few years ago. Lower grocery prices help, but they don’t offset rent increases, higher mortgage payments, or rising insurance premiums. Wage growth has also been uneven. While higher earners and specialized professionals have seen meaningful pay gains, many middle-income and hourly workers find that modest raises are quickly absorbed by fixed expenses. Even as inflation cools on paper, households budgeting month to month may feel little practical difference in their financial breathing room. This disconnect fuels public skepticism around the idea of an “economic recovery.” When families still rely on credit cards to cover routine expenses or delay major purchases due to uncertainty, positive economic indicators can feel abstract or disconnected from reality. Improvements are often incremental — and easily outweighed by one unexpected bill. Economists note that sustained relief takes time, especially after a period of prolonged price increases. While signs of stabilization are emerging at grocery stores and gas stations, many households remain in a catch-up phase, working to rebuild savings and regain control over their budgets. Until broader costs come down or incomes rise more decisively, the recovery will continue to feel slower than the data suggests.

Americans Are Falling Behind Less — New Data Shows Credit-Card Delinquencies May Be Stabilizing

After two years of steadily rising household financial strain, a new batch of data suggests the pressure may finally be easing. According to analysts reviewing recent Federal Reserve and commercial bank reports, consumer-debt delinquency rates — especially on credit cards — appear to be leveling off after months of sharp increases. It’s a tentative shift, but one that could signal that American households are regaining some ability to manage their monthly bills. Economists attribute this improvement to a handful of converging factors. Wage growth has remained steady, and hiring continues to hold up enough to support household cash flow. Some families have also adjusted their budgets after a year of elevated prices, trimming discretionary spending to keep up with core obligations. These shifts, while modest, have helped prevent delinquencies from climbing further. Still, the picture is far from universally positive. Analysts caution that delinquencies have not fallen back to pre-pandemic levels — they have simply stopped getting worse. Many households continue to carry record-high balances, and the share of borrowers with little to no emergency savings remains significant. In other words, the stabilization is real, but it’s fragile. Lenders, meanwhile, remain watchful. Banks have reported that although missed payments are no longer spiking, customers are taking longer to pay down their balances. Some issuers have tightened credit standards or increased monitoring of higher-risk accounts. These moves reflect a recovery still in its early stages — one that could easily reverse if job growth weakens or borrowing costs stay elevated. For now, the takeaway is cautiously optimistic: Americans may be turning a corner on the worst of their credit-card stress. But with balances still high and savings thin, the path forward depends heavily on whether wages hold steady, inflation continues to cool, and interest-rate cuts materialize in the months ahead.

A $6.25 Billion Bet on Tomorrow — Michael & Susan Dell Back “Trump Accounts” for 25 Million U.S. Children

Michael and Susan Dell have pledged a record-setting $6.25 billion to support the new national “Trump Accounts” program designed for children born between 2025 and 2028. Under the plan, each eligible child receives $1,000 from the Treasury in a tax-advantaged investment account. The Dells’ contribution will extend access to roughly 25 million children who fall outside the initial eligibility window, adding approximately $250 per child — a financial boost intended to seed early wealth creation. While the scale of the pledge is extraordinary, it aligns with a long philanthropic trajectory. The Michael & Susan Dell Foundation, established in 1999, has historically focused on children’s issues and community initiatives in the United States, India, and South Africa. Over the past two decades, the foundation has distributed more than $650 million to improve educational access, health outcomes, and family economic stability, and manages more than $466 million in assets today. In recent years, its global development financing has continued to rise, reflecting a sustained commitment to children and opportunity. Supporters view the latest gift as a forward-looking investment in economic mobility, offering children the chance to accumulate real assets from an early age that can grow into funding for higher education, homeownership, or entrepreneurship. By shifting the timeline of financial empowerment to childhood, the initiative aims to narrow long-standing wealth and opportunity gaps. Critics counter that while investment accounts may help families in the long term, they do little to address urgent problems facing children today — from hunger and housing insecurity to systemic poverty. Some also caution that relying on billionaire-backed investment structures risks moving essential social welfare responsibilities away from public institutions and into private hands. As the largest private commitment to U.S. children in decades, the Dell contribution signals a powerful moment. Whether it becomes a new model for building generational wealth or ignites a broader national debate about the role of philanthropy in public life will unfold over time. What remains undeniable is the program’s potential to reshape financial futures for millions of today’s children — giving them a meaningful head start on the road to stability, opportunity, and lifelong prosperity.

Is Gray the New Black Friday?

Black Friday has long been celebrated as the biggest spending day of the year — a symbol of door-buster chaos, deep discounts and overflowing carts. But this year, a different tone is emerging. Economic uncertainty, higher prices, and cautious consumer sentiment are reshaping the holiday shopping landscape, leading many to wonder whether the frenzy is fading and a new era of measured, selective spending has arrived. Industry forecasts project that total U.S. holiday sales could exceed the $1 trillion mark for the first time. But growth estimates tell a more complex story, rising only modestly from last year and reflecting the tension between aspiration and reality. Shoppers are spending, but with far more restraint. And while analysts point to consumer resilience, many families are navigating inflation, job pressure and reduced financial confidence — and their buying behaviors are shifting accordingly. The Readovia Perspective The optimistic sales forecasts may not fully align with the economic mood on the ground. After the government shutdown and months of escalating economic stress, we question whether predictions of record-breaking consumption can hold. A holiday season built on tighter budgets and intentional decisions feels more believable than one defined by runaway spending. That shift is transforming Black Friday itself. Instead of chasing massive markdowns and impulse buys, shoppers are comparing more aggressively, delaying decisions and prioritizing purpose. Discounts are smaller, inventory moves slower and consumers are increasingly willing to walk away. The winners this year won’t be the loudest or the cheapest retailers — they’ll be the ones offering real value, trustworthy quality and clear reasons to buy. For many, Black Friday has become less about splurge-driven celebration and more about strategic planning. The new shopping strategy: buy what truly matters, not whatever flashes in a banner ad. A slower, steadier and more intentional rhythm is emerging — and in many ways, it reflects where the country stands right now. Maybe gray is the new Black Friday. We’ll be watching.

Alphabet Shares Surge After Berkshire Makes Rare $4.9 Billion Investment

Alphabet Inc. shares rallied more than 5 percent on Monday after Berkshire Hathaway revealed a multi-billion-dollar equity stake in the tech giant. The investment, estimated at nearly $5 billion, represents one of the largest new positions taken by the conglomerate in recent years and arrives at a pivotal moment for the artificial intelligence race. The purchase adds approximately 17.85 million Alphabet shares to Berkshire’s portfolio and marks a notable move into the technology sector for the firm long known for its caution around companies perceived as difficult to project or value. The entry signals renewed confidence in Alphabet’s ability to evolve its business model amid accelerating competition in AI infrastructure and cloud computing. Market analysts say the investment reflects growing investor conviction in Alphabet’s long-term strategy, pairing its dominant digital-advertising business with major advances in generative AI, enterprise tools, and next-generation data systems. The move also comes as Alphabet intensifies spending to expand its computing capacity and AI-focused research pipelines. The market reaction was swift, with trading volume surging as investors interpreted the stake as a high-profile endorsement of Alphabet’s competitive positioning and growth prospects. The decision may also represent one of the final large commitments initiated under Warren Buffett’s leadership as Berkshire prepares for an eventual transition in senior management. Attention now turns to how Alphabet plans to deploy its strengthened market momentum, particularly in scaling its AI development roadmap and cloud expansion. Investors will be watching for updates on capital spending, revenue diversification beyond advertising, and competitive responses from other major technology companies in the months ahead.

The Relief Didn’t Last — Wall Street Slides as Tech Stocks Drop

The stock market’s brief rebound lost momentum today as major indexes fell sharply on growing doubts that the Federal Reserve will cut interest rates in December. The earlier bounce — largely driven by investor relief after the government shutdown ended — has now reversed, with the Nasdaq Composite falling roughly 1.44%, the S&P 500 dropping around 1.09%, and the Dow slipping about 1.24%. The decline follows a short-lived “relief rally,” a temporary jump in stock prices driven more by emotional optimism than by real economic improvement. The reversal was led by a sell-off in major technology stocks, including Nvidia, Palantir and Tesla — companies that have fueled much of 2025’s market momentum but now appear vulnerable to valuation pressure and profit-taking. Investors reacted sharply to new commentary from Federal Reserve officials who signaled that inflation remains too elevated to justify easing monetary policy, dampening expectations of a December rate cut that many traders had been counting on to support growth sectors such as AI and automation. Market strategists say this marks a meaningful psychology shift. After months of enthusiasm and momentum trading centered around artificial intelligence, investor behavior now appears to be rotating toward more defensive positioning and renewed focus on valuation discipline. Analysts say the momentum trade may be starting to unwind — a sign that speculative bets are giving way to fundamentals-based decision-making. The implications reach beyond Wall Street trading desks. For business leaders planning budgets, capital spending and hiring strategies based on expectations of cheaper borrowing, today’s market move is a reminder that the cost of money still matters — and so does pacing. Companies overly reliant on rapid-acceleration growth models or market optimism may find themselves needing to adjust expectations and risk tolerance. For investors and industry observers, today’s pullback may not simply signal a correction, but rather the beginning of a broader recalibration. The age of effortless gains may be ending — and the era of intentional, disciplined strategy may be returning. Momentum may move markets for a season, but fundamentals determine who lasts.