Fixed vs. Adjustable-Rate Mortgages: Why Fixed Loans Are the Safest Bet for Most Buyers

Buying a home is one of the largest financial decisions most people will ever make. Yet one of the most important choices buyers face — fixed-rate versus adjustable-rate mortgages — is often misunderstood or rushed through during the excitement of house hunting. While adjustable-rate mortgages (ARMs) can look appealing at first glance, fixed-rate mortgages remain the safest and most predictable option for the vast majority of homebuyers. Here’s why. The Key Difference, Explained Simply A fixed-rate mortgage locks in your interest rate for the life of the loan. Your monthly principal and interest payment never changes, regardless of what happens in the broader economy. An adjustable-rate mortgage, on the other hand, starts with a lower introductory rate for a set period — often five, seven, or ten years — before adjusting periodically based on market conditions. Once that adjustment period begins, your payment can rise significantly. On paper, ARMs can look cheaper. In real life, they often introduce risk that many homeowners are unprepared for. Why Predictability Matters More Than a Low Introductory Rate Housing costs don’t exist in a vacuum. Property taxes rise. Insurance premiums increase. Maintenance costs are unpredictable. A fixed-rate mortgage removes at least one major variable from the equation. With a fixed loan: Your interest rate stays the same Your principal and interest payment remain stable Budgeting becomes easier Long-term planning is clearer Worth Noting If your property taxes and homeowners insurance are rolled into your monthly mortgage payment through an escrow account, that total payment can still increase over time. This typically happens when taxes or insurance premiums rise — not because your mortgage rate has changed. Even so, locking in a fixed interest rate protects the largest and most volatile portion of your housing cost, which is why fixed-rate loans continue to offer greater peace of mind for most buyers. The Hidden Risk of Adjustable-Rate Mortgages ARMs are often marketed with the promise that homeowners can refinance before the rate adjusts. But refinancing is never guaranteed. It depends on: Interest rate conditions Home values Credit scores Income stability Is Refinancing Guaranteed? If rates rise sharply or a borrower’s financial situation changes, refinancing may not be possible — leaving homeowners exposed to higher payments at exactly the wrong time. In many cases, ARM borrowers are betting on the future. Fixed-rate borrowers are planning for it. When an Adjustable Rate Might Make Sense There are limited situations where an ARM can be reasonable. These include: Buyers who are certain they will sell within a short time frame Households with significant financial buffers Investors using short-term financing strategies Weighing In Even if an ARM appears feasible, the risks should be clearly understood. For most families planning to stay in their homes for years, the potential downside often outweighs the initial savings. The Bottom Line A fixed-rate mortgage isn’t about chasing the lowest possible payment today. It’s about protecting yourself from uncertainty tomorrow. For buyers who value stability, long-term planning, and peace of mind — especially first-time homeowners — fixed-rate mortgages remain the safest and most responsible choice.

7 Quiet Money Moves Americans Are Making in 2026

While headlines often spotlight market swings, rate speculation, and headline-grabbing trends, many Americans are making quieter financial adjustments in 2026 — moves that don’t draw attention but may prove far more consequential over time. 1. Moving idle cash into accounts that actually earn Rather than letting money sit in low-interest checking accounts, more Americans are shifting cash into modern savings and cash-management options that generate meaningful returns while remaining accessible. This includes money-market accounts, certificates of deposit, and app-based tools such as Cash App’s savings feature, which currently offers a 3.25% yield. These quiet optimizations can add up without adding complexity. 2. Parking cash more intentionally Instead of constantly chasing the highest advertised yield, savers are prioritizing stability and simplicity. Fewer accounts, clearer access to funds, and predictable returns are increasingly valued as uncertainty around rate cuts and economic direction lingers. 3. Trimming expenses without formal “budgeting” Rather than rigid budgets, households are cutting recurring costs that quietly piled up over the years. Subscription clean-ups, fewer impulse purchases, and more mindful spending habits are becoming routine — even among higher earners. 4. Staying put in housing With home prices still elevated and mortgage rates easing unevenly, many homeowners are choosing patience over movement. Renovations, refinancing strategies, and long-term planning are replacing the once-common urge to upgrade quickly. 5. Reframing side income as protection, not identity Side hustles remain widespread, but the motivation behind them is shifting. Extra income is increasingly viewed as a financial cushion rather than a lifestyle badge. Instead of chasing constant growth, many are using side income to offset inflation, strengthen savings, or create flexibility — without turning every spare hour into a second career. 6. Rebuilding emergency funds with renewed urgency Emergency savings have re-entered the financial spotlight. Surveys show Americans heading into 2026 with a renewed focus on cash buffers, often using automation and higher-yield savings tools to rebuild financial resilience after several volatile years. 7. Treating debt reduction and credit health as strategy With credit card rates still elevated, paying down high-interest debt has become a proactive financial move rather than a reactive one. Improving credit scores, lowering balances, and strengthening borrowing profiles are increasingly seen as long-term investments in financial flexibility. The Wallet Perspective None of these moves feel dramatic — and that’s the point. In 2026, financial confidence is being built less through bold bets and more through restraint, structure, and intention. Americans aren’t abandoning ambition; they’re just giving it a seatbelt. Instead of chasing short-term wins, many are quietly building foundations sturdy enough to handle whatever comes next — without needing to check the market every five minutes.

Household Budgets Tighten as Everyday Costs Continue to Outpace Wage Growth

For many American households, the pressure on monthly budgets is no longer coming from one big expense, but from a steady accumulation of higher everyday costs. Groceries, utilities, insurance, and basic services continue to rise, leaving families with less flexibility even as inflation cools in headline numbers. Consumers report that routine purchases now require more planning, with many cutting back on discretionary spending to absorb higher essentials. Items once considered stable parts of a household budget—such as food staples and home utilities—have become less predictable, forcing families to rework spending priorities month by month. While wages have increased in some sectors, they have not kept pace with the cumulative impact of ongoing price increases. Financial planners note that this imbalance is pushing more households to rely on budgeting tools, short-term savings strategies, and stricter spending controls just to maintain stability. Retailers and service providers are also adjusting, offering smaller package sizes, subscription pricing, and targeted discounts as consumers become more price-sensitive. The shift signals a broader change in spending behavior, with value and necessity outweighing convenience and brand loyalty. As 2026 unfolds, the American wallet is being shaped less by economic headlines and more by lived experience—where managing everyday costs has become a central financial skill rather than an occasional concern.

Tax Season 2026: What’s Changing for Your 2025 Return

Tax season is arriving with a clear message from Washington: the government wants refunds and payments moving faster, safer, and more digitally than ever. For Americans filing 2025 tax returns in 2026, several updates stand out—not because they’re complicated, but because they change what “normal” looks like when you’re expecting a refund or planning deductions. The biggest operational shift is how refunds are delivered—and it’s coming straight from the top. An Executive Order signed by Donald Trump directs federal agencies to modernize payments to and from Americans by moving away from paper-based systems. In line with that order, the IRS is phasing out paper refund checks for individual taxpayers, steering filers toward direct deposit and other electronic payment methods designed to reduce fraud, delays, and administrative costs. Policy changes are also landing just as millions of households file. One of the most notable is a new deduction for car loan interest introduced under the One Big Beautiful Bill (OB3). Treasury and IRS guidance outlines a deduction that may apply even if you take the standard deduction, potentially benefiting taxpayers who purchased eligible new, made-in-America vehicles in 2025—subject to income limits and other qualifications. Even the basics have shifted. For the 2025 tax year, the standard deduction is higher across all filing statuses, and eligible seniors may qualify for an additional deduction under new rules. These changes mean taxable income calculations could look different for many filers before credits and other deductions are even factored in. The practical takeaway is simple: if you expect a refund, now is the time to ensure your electronic payment information is up to date. And if you made major financial decisions in 2025—such as buying a vehicle or transitioning into retirement—it’s worth taking a closer look at what you may newly qualify for. This tax season isn’t just about filing—it’s about adapting to a system that’s rapidly going digital.

The One Question Entrepreneurs and Side Hustlers Can’t Afford to Ignore in 2026

Entrepreneurs and side-hustlers don’t usually struggle with effort. They struggle with alignment. Days fill quickly with planning, posting, refining, researching, and building — yet the financial results don’t always reflect the work being done. Busy days can still end without progress where it matters most. The issue isn’t ambition or discipline. It’s that too much work never actually touches revenue. Tasks feel productive, but they don’t move money. Over time, that disconnect creates frustration, burnout, and the sense that something isn’t working — even when effort is constant. One question helps cut through that noise: how does today’s work connect to revenue? Not eventually. Not after everything is perfect. Today. When that question becomes part of daily decision-making, priorities shift. Work becomes more intentional. Time is spent differently. Revenue-connected work doesn’t always mean selling directly. It can mean pitching, following up, improving a conversion point, promoting something already built, onboarding a client, or refining a monetized page. The common thread is simple: the action creates a clear path between effort and income. The power of this approach compounds over time. One revenue-focused action per day may feel small, but over the course of a year, it adds up to 365 intentional actions tied directly to earning. Imagine that. Few businesses fail because they didn’t work hard enough. Many stall because too few days were spent doing work that actually moved money. Consistency in the right direction beats intensity without focus — every time. The Takeaway Before the day ends, ask one question: How did today’s work connect to revenue? Then make sure at least one action answers it clearly. Progress isn’t built all at once. It’s built daily — one intentional, revenue-connected task at a time. ——————– Recommended: The Skills That Will Matter More Than Capital in 2026

Powerball Jackpot Soars To $1.7 Billion

The U.S. Powerball jackpot has climbed to an astonishing $1.7 billion, setting the stage for a record-setting Christmas Eve drawing that has captured attention nationwide. The latest round of play produced no jackpot winner, allowing the prize to swell further after Monday night’s drawing. Several tickets matched five numbers to secure million-dollar wins, but the grand prize remains unclaimed — and growing. The odds of winning remain extraordinarily slim, roughly 1 in 292 million, yet the holiday timing has fueled ticket sales and renewed enthusiasm. Winners will ultimately face a choice between a long-term annuity paid out over decades or a one-time cash option estimated at just over $780 million, a sum that would instantly reshape any financial reality. The current jackpot ranks among the largest in U.S. lottery history, joining a short list of billion-dollar Powerball runs that have captured the public imagination. In a year marked by economic uncertainty and rising costs, the swelling jackpot has become a shared moment of optimism — a reminder of possibility, however remote. Beyond the headline figure, the extended rollover highlights the unique tension at the heart of lottery culture: the promise of sudden transformation set against the certainty of long odds. With the next drawing scheduled for Christmas Eve, millions of Americans may head into the holiday holding a ticket — and a fleeting sense of what-if — as the year comes to a close.

Democrats & Republicans Pitch Competing Plans to Tackle America’s Affordability Crisis

As the cost of living continues to stretch household budgets, lawmakers on Capitol Hill are rolling out competing proposals aimed at lowering expenses for millions of Americans. With affordability emerging as one of the dominant political issues heading into 2026, both parties are trying to claim the mantle of economic relief — but with sharply different approaches. Democrats are pushing a plan centered on reducing out-of-pocket costs for everyday essentials, including efforts to lower prescription drug prices, expand housing assistance and boost subsidies for child care. They argue that household budgets have endured years of inflation-driven pressure and need immediate, direct support. Republicans, meanwhile, are prioritizing tax relief and deregulation. Their proposal focuses on easing federal rules they argue drive up prices, while offering targeted tax credits aimed at working families and small businesses. GOP leaders say the fastest way to bring down costs is to reduce the government’s footprint and spur private-sector growth. Households Still Feeling the Strain Despite slowing inflation and brighter economic indicators in some areas, many Americans say their financial stress hasn’t eased. Rising rents, higher insurance premiums, lingering food costs, and elevated interest rates continue to weigh heavily on families — especially lower-income consumers who face the steepest trade-offs. A Political Battle With Real Stakes With both chambers looking ahead to a contentious 2026 election season, lawmakers are racing to present solutions that resonate with voters. While the two plans share the same goal — improving affordability — the divide over how to get there has set the stage for months of negotiations. For now, Americans are watching closely, hoping the gridlock breaks and real relief finally reaches their wallets.

Tesla Shares Surge on Confirmation of Driverless Robotaxi Testing

Tesla shares jumped sharply Monday after CEO Elon Musk confirmed the company is testing fully driverless robotaxis on public roads without onboard safety monitors, a development that reignited investor optimism around Tesla’s long-term autonomous vehicle ambitions. The stock climbed to its highest level in nearly a year, reflecting renewed confidence among traders and long-term shareholders who see autonomous technology as a key driver of Tesla’s future valuation. The surge pushed the company’s market capitalization higher as investors reacted to what they viewed as tangible progress toward full autonomy. Tesla’s robotaxi initiative is central to Musk’s broader vision of transforming the company beyond electric vehicle manufacturing and into a leader in autonomous transportation and robotics. Earlier testing phases included human safety monitors, making the confirmation of unsupervised testing a significant milestone in the program’s evolution. Still, analysts remain divided. While advances in autonomy continue to fuel bullish expectations, concerns around electric vehicle demand, regulatory hurdles, and execution risks persist. Monday’s rally underscores how quickly market sentiment can shift when Tesla signals progress on its most closely watched technologies.

IRS Staffing Shortages Could Make the 2026 Tax Season a Rough One

As Americans prepare for the upcoming tax season, growing concerns are emerging over the Internal Revenue Service’s ability to handle the workload. Deep staffing reductions across the agency, including reports that some departments are operating with as little as one-third of their normal workforce, are raising red flags about delays and service disruptions in 2026. The IRS has lost a significant number of employees over the past year through retirements, buyouts, and budget-driven cuts. While workforce reductions have affected the agency broadly, internal operations tied to taxpayer assistance, return processing, and backend support have been hit particularly hard. The timing is notable, coming just as tax filings are expected to rise and rules continue to grow more complex. Fewer staff members could translate into longer wait times for taxpayers seeking help, slower processing of returns, and delays in issuing refunds. Call centers may struggle to keep up with demand, and taxpayers facing issues or errors could find it harder to reach a live representative during critical filing windows. The strain may also extend beyond customer service. Reduced staffing could limit the agency’s ability to conduct audits, resolve disputes, and manage compliance efforts efficiently, potentially affecting both revenue collection and enforcement consistency. For taxpayers, the message heading into 2026 is one of caution and preparation. Filing early, double-checking returns, and avoiding last-minute submissions may become more important than ever as the IRS navigates a tax season with fewer resources and rising demands.

Why Falling Inflation Still Isn’t Showing Up in Everyday Household Budgets

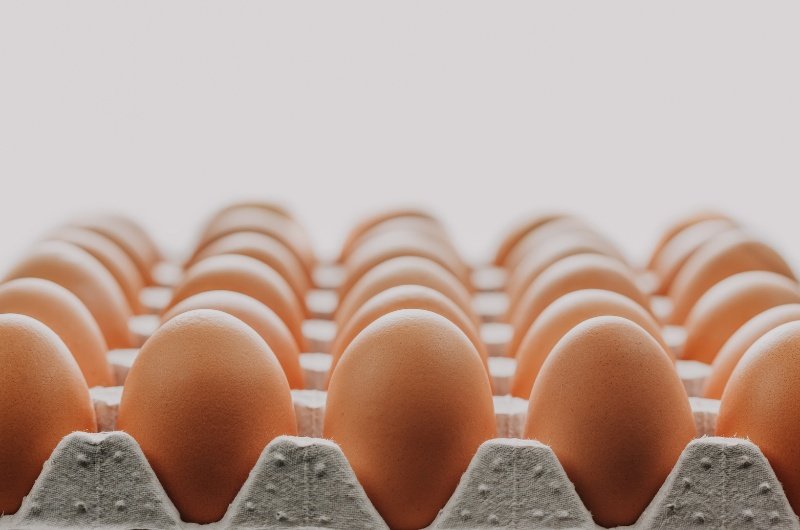

Inflation has eased from its recent highs, and in some cases, prices are clearly coming down. At one point, the price of eggs felt like a runaway train, racing ahead of household budgets and turning a basic necessity into a talking point. Now, we’re seeing eggs priced under two dollars a dozen. But for many households, that hasn’t translated into a real sense of financial relief. The reason is simple: while certain items have become more affordable, the underlying cost structure of daily life is still elevated. Housing, insurance, utilities, healthcare, childcare, and interest payments continue to consume a larger share of household income than they did just a few years ago. Lower grocery prices help, but they don’t offset rent increases, higher mortgage payments, or rising insurance premiums. Wage growth has also been uneven. While higher earners and specialized professionals have seen meaningful pay gains, many middle-income and hourly workers find that modest raises are quickly absorbed by fixed expenses. Even as inflation cools on paper, households budgeting month to month may feel little practical difference in their financial breathing room. This disconnect fuels public skepticism around the idea of an “economic recovery.” When families still rely on credit cards to cover routine expenses or delay major purchases due to uncertainty, positive economic indicators can feel abstract or disconnected from reality. Improvements are often incremental — and easily outweighed by one unexpected bill. Economists note that sustained relief takes time, especially after a period of prolonged price increases. While signs of stabilization are emerging at grocery stores and gas stations, many households remain in a catch-up phase, working to rebuild savings and regain control over their budgets. Until broader costs come down or incomes rise more decisively, the recovery will continue to feel slower than the data suggests.